Sentiment-Driven Insights for U.S. Equity Markets

Academic

This project started with a simple question:

Does public sentiment actually move markets — or does it just react to them?

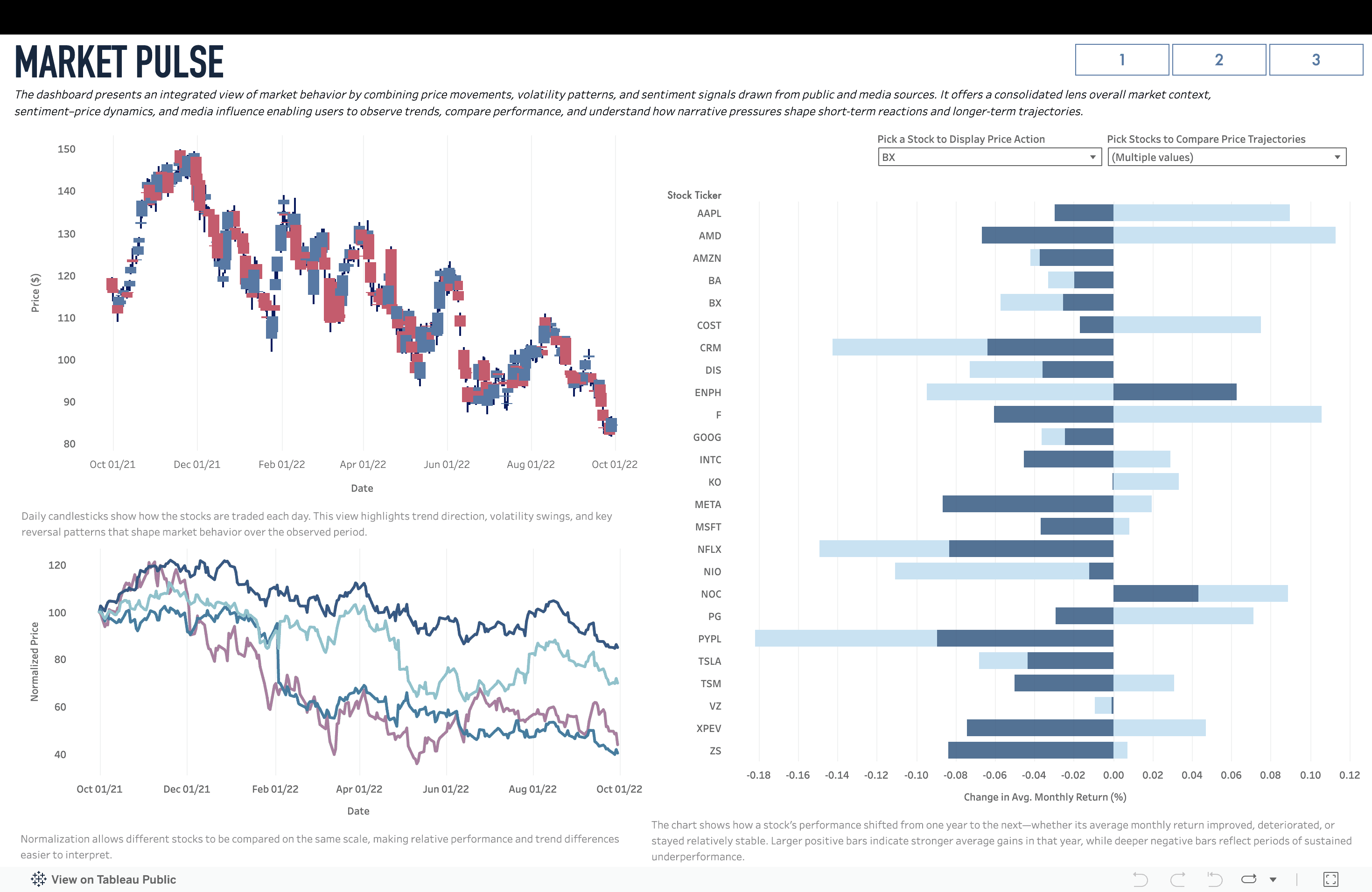

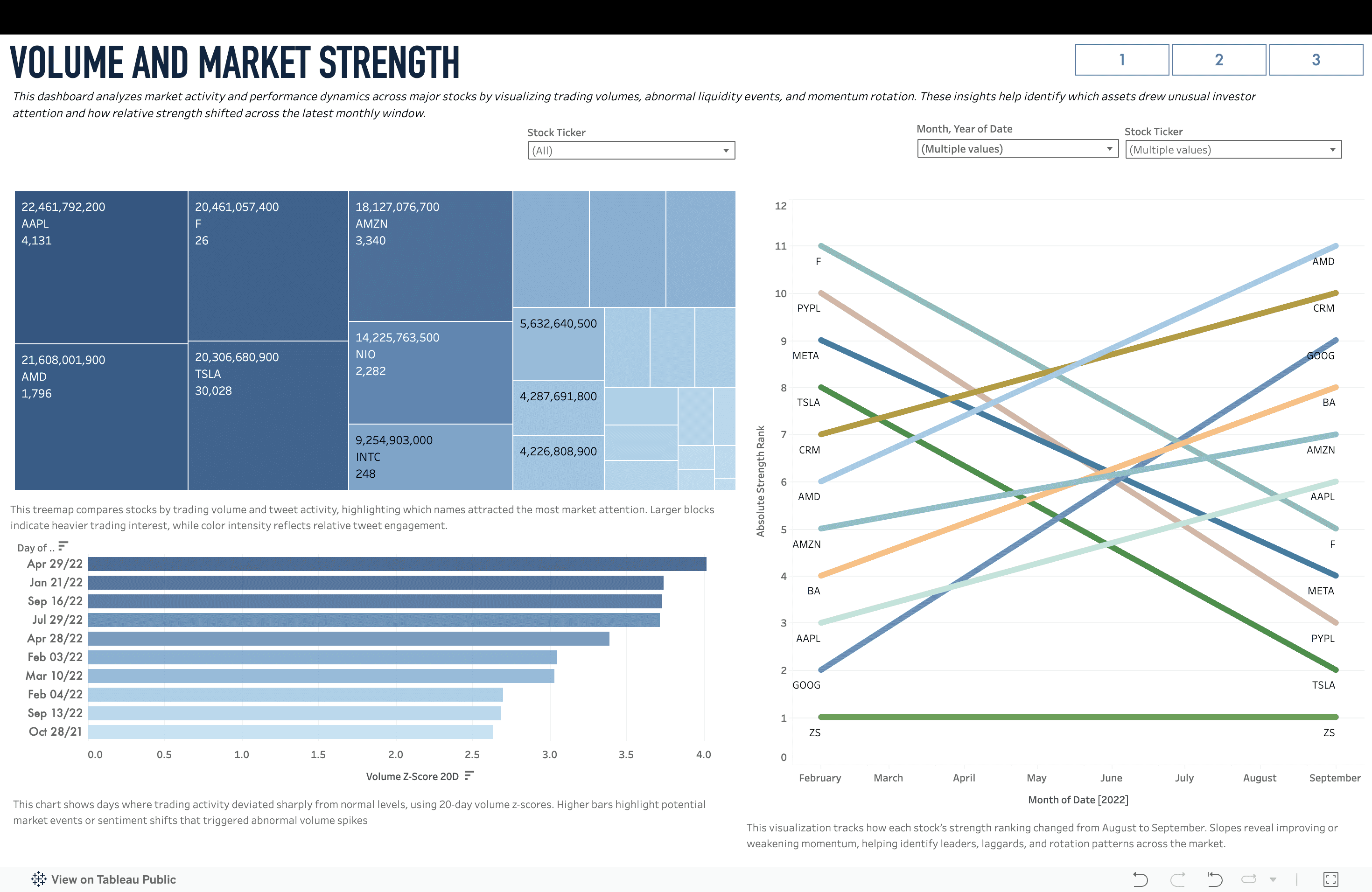

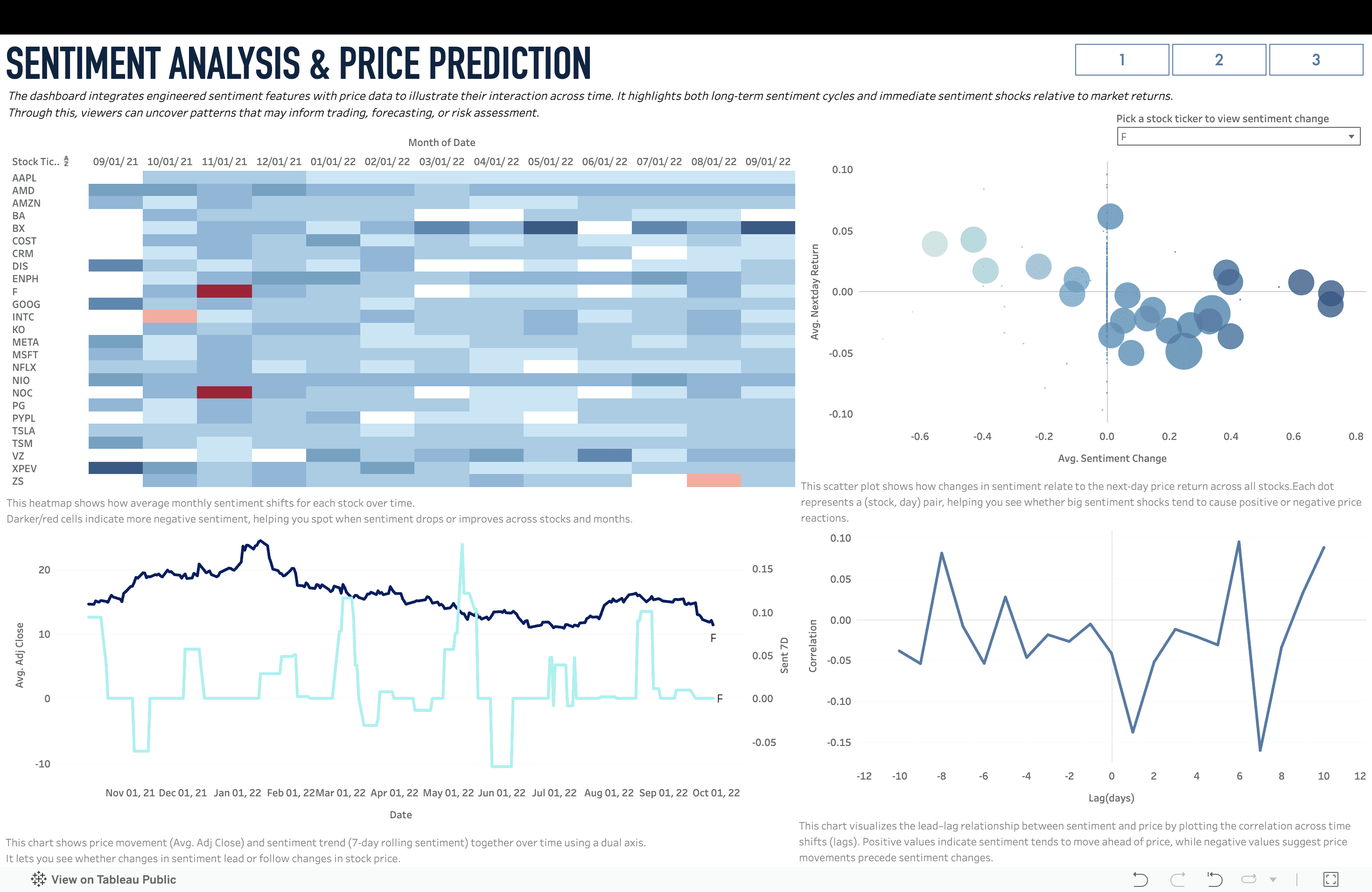

For this analysis, I built an end-to-end pipeline combining Twitter sentiment with historical price data for 25 U.S. equities. Using Python (RoBERTa + VADER for sentiment scoring), I engineered financial features like rolling volatility, volume Z-scores, and relative strength ranks. The cleaned dataset was then modeled and visualized through three interactive Tableau dashboards.

Click here to access the project!

The goal wasn’t just to “predict price.” It was to understand behavior.

Across the dashboards, a few patterns stood out:

Sentiment–return alignment was noticeably stronger on high-volume trading days.

Sharp sentiment shocks often coincided with abnormal liquidity events.

Lead–lag analysis showed that sentiment sometimes preceded short-term price reactions — but not consistently enough to act as a standalone signal.

The takeaway?

Sentiment works best as a confirmation layer, not a forecasting oracle.

This project was completed as part of MGTA 457 – Business Intelligence Systems at UC San Diego (Rady School of Management).